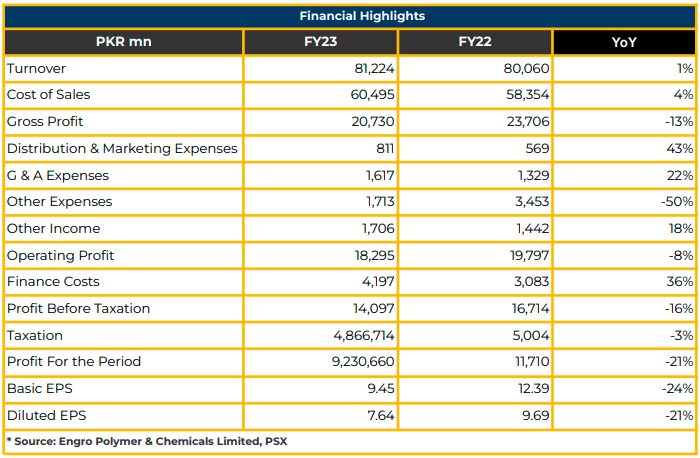

In CY23, EPCL experienced a substantial 21% YoY decline in net profits, amounting to PKR 9.23 billion (EPS: PKR 9.45), marking a significant decrease from the prior year’s PKR 11.71 billion (EPS: PKR 12.39).

Concurrently, the cost of sales witnessed a 4% YoY increase to PKR 60.49 billion during this period, with the company attributing the decline in profitability to factors such as increased inflation, devaluation, lower core delta, and adverse budgetary impacts.

The company’s total revenue reached PKR 81.22 billion, reflecting a 1% YoY decline from the preceding year. Segment-wise, PVC generated PKR 69.81 billion, and Chlor Alkali contributed PKR 11.03 billion.

Profitability was distributed as follows: PVC at PKR 6.24 billion, Chlor Alkali at PKR 2.62 billion, and others at PKR 69 million in CY23.

In the same period, EPCL sold 221KT of PVC, a decrease from the previous year’s 241KT in CY22. The domestic PVC market faced challenges due to political uncertainty, reduced construction activity, higher inflation, and devaluation.

Similarly, EPCL sold 66KT of liquid and 12KT of Flakes (Total of 78KT of Chlor Alkali), 3% higher than the previous year. Notably, EPCL reported a surge in exports to USD 26 million, marking a 20% YoY increase.

Simultaneously, gross profit decreased by 13% YoY to PKR 20.73 billion from PKR 23.71 billion in the same period last year. On the global front, Chlor Alkali prices remained under pressure due to oversupply. domestic market margins improved, driven by a favorable textile export market, leading to an overallpickup in caustic demand in 2HCY23. Supply to the domestic Export-Oriented sector was maintained at 78% in CY23.

PVC international prices remained within the range of USD 770-850 per MT in CY23 due to lackluster markets post-scheduled maintenance bottoming out in October.

The market breakdown for PVC applications in CY23 was: Fittings (55%), Film & sheet (15%), Profile (8%), Cable Compound (8%), Shoe (6%), Flexible Hose (5%), Others (3%).

Ethylene prices experienced volatility due to instability in the global and gas markets in CY23. Starting March, Ethylene prices began to rise due to supply tightness and an increase in crude prices. Operating rates of steam crackers declined to 78% during the year.

Lackluster downstream PPE demand led to prices remaining rangebound once supply disruptions eased. Management shared that the Hydrogen Peroxide project’s completion is expected in 2QCY24.

The management highlighted that the availability of gas at competitive prices remains a key challenge. EPCL experienced fluctuations in gas rates and availability in CY23, leading to an agreement with SSGC for uninterrupted gas supply at a blended rate of 25:75 from August to November 2023. In December, the RLNG blended ratio was revised upwards to 40:60 for captive and 20:80 for industrial gas.

Despite a significant 50% decline, other expenses totaled PKR 1.71 billion in CY23, down from PKR 3.45 billion the previous year. Meanwhile, other income increased by 18% YoY to PKR 1.71 billion in CY23.

Due to higher policy rates, EPCL’s finance costs rose 36% YoY to PKR 4.20 billion from PKR 3.08 billion. Profit before taxation decreased by 16% YoY to PKR 14.10 billion in CY23, with taxation declining by 3% YoY to PKR 4.87 billion during the same period. Concerning dividends, the management emphasized the priority of stabilizing markets before considering payout.

Going forward, the company anticipates operational sustainability and timely completion of ongoing projects. Economic stability is expected to support operations. However, bearish international prices due to oversupply might continue to impact PVC sales.

Domestically, the construction sector is expected to rebound after the elections. Additionally, higher crude oil prices might increase ethylene prices to USD 1,000 per ton. The management anticipates improving margins in 2HCY24 due to the strengthening of demand.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.