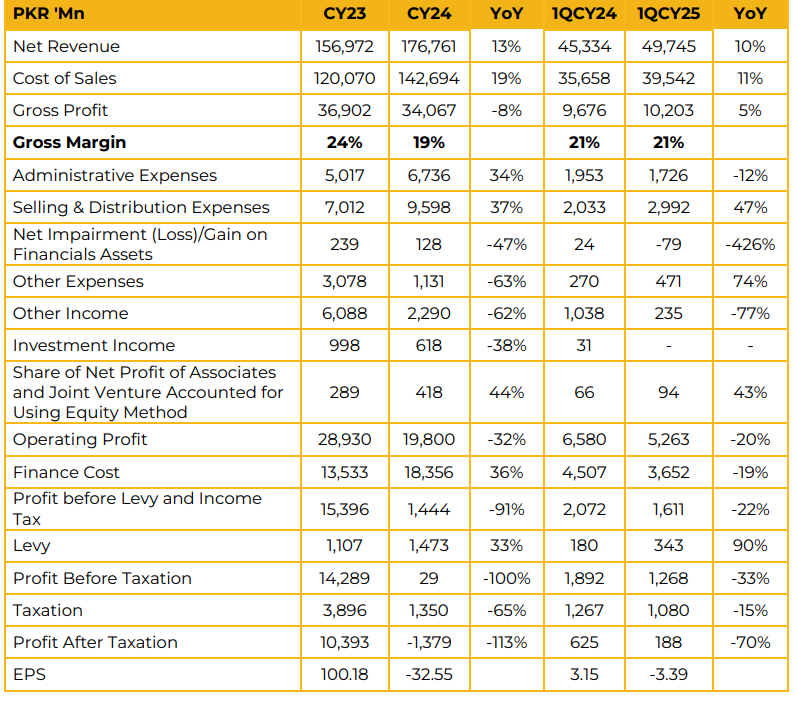

Packages Limited reported an unconsolidated net profit of PKR 1.91 billion (EPS: PKR 20.68) for CY24, reflecting a notable decline from PKR 2.78 billion (EPS: PKR 30.37) in the previous year. This drop in profitability was primarily due to the absence of dividend income from Bulleh Shah Packaging (Private) Limited in the current year. Overall, dividend income stood at PKR 4.06 billion in CY24, down from PKR 5.84 billion in CY23.

Additionally, the finance cost rose to PKR 1.59 billion, driven by long-term borrowings to finance investments in group companies, including StarchPack (Private) Limited, Tri-Pack Films Limited, and Hoechst Pakistan Limited. In CY24, PKGS injected PKR 3 billion and PKR 8 billion into StarchPack and Bulleh Shah Packaging, respectively. Among subsidiaries, Packages Converters (Pvt) Limited posted net sales of PKR 49.1 billion, down 1% YoY, with sales split as 25% from folding carton, 32% from consumer products, and 43% from flexible packaging. Bulleh Shah Packaging reported a 2% YoY decline in revenue to PKR 57.9 billion, with PKR 52 billion from the paper & board division and PKR 19 billion from corrugated packaging. DIC Pakistan Limited reported a 10% YoY rise in sales to PKR 11.7 billion.

Packages Real Estate posted PKR 6 billion in sales, up 10% YoY. Omyapack’s revenue increased 31% YoY to PKR 2.1 billion. Tri-Pack Films posted sales of PKR 29.4 billion, reflecting 18% growth, supported by the addition of a new BOPP production line. Tri-Pack is also exploring exports and expects improved profitability going forward. StarchPack (Pvt) Limited, which began commercial operations in 1QCY24, reported a significant rise in revenue to PKR 3.6 billion from PKR 52.4 million in SPLY. The company expects to break even by the end of CY25, with results already improving in 1QCY25. Hoechst Pakistan Limited delivered 25% YoY sales growth to PKR 26.8 billion and reported pre-tax profit of PKR 3.5 billion, supported by higher volumes and deregulation of nonessential product prices. Packages Lanka (Pvt) Limited posted profit before tax of LKR 1 billion, up 23% YoY, while Packages Trading FZCO earned AED 1.8 million in profit before tax on sales of AED 105.9 million. The company is actively engaging with the government and FBR regarding anti-dumping duties, previously imposed for five years on paper, folding boxes, and flexible packaging.

These duties have now lapsed, and an application for renewal is under review by the National Tariff Commission. Packages Limited is also pursuing anti-circumvention measures and has filed with the Ministry of Commerce and FBR. Last year, a 10% regulatory duty on paper and board imports was imposed but it has been reversed. Antidumping duties remain in place at 28%, along with a 10% import duty.

Margins in 4QCY24 declined due to lower orders from key clients—top ten customers account for 75% of turnover—alongside seasonal factors, low inventory levels in last quarter. The FY24 budget imposed additional formal sector taxes, negatively affecting the outlook for the liquid packaging segment. Going forward, raw material prices are expected to remain stable due to a favorable crop this year. The company anticipates EBITDA growth, with a positive bottom line expected for StarchPack at the start of next year.

For Bulleh Shah, major capex has been completed, and no significant expenditure is expected from CY26 to CY28. Profitability is expected to improve once capacity utilization rises. The NTC decision on anti-circumvention is expected within one quarter. The company has no plans for a stock split. The company aims to expand its brown board portfolio, utilizing a newly installed 100,000-ton corrugated plant. Management emphasized that if the government provides relief to the salaried class through budgetary measures, it would directly boost their purchasing power, thereby increasing demand for the company’s packaged goods.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose