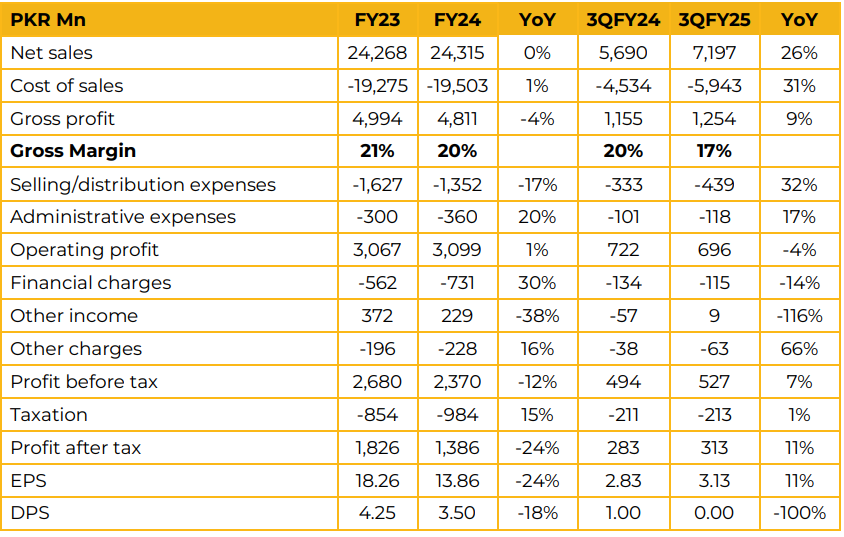

Ittehad Chemicals Limited reported earnings per share of PKR 13.86 in FY24 against earnings per share of PKR 18.26 in FY23 a decrease of 24%.

Total revenue in FY24 reached PKR 24.3 Bn remaining stagnant compared to FY23 with PKR 24.3 Bn. The company saw its gross margin decrease from 21% in FY23 to 20% in FY24. In this fiscal year the company has seen its margin further deteriorate to 17% in 3QFY25. This was due to the increase in energy costs. However, net revenue in 1QFY25 was PKR 7.2 Bn, up 26% from PKR 5.7 Bn in 1QFY24.

As a result, earnings per share rose 11% from PKR 2.83 in 1QFY24 to PKR 3.13 in 1QFY25. The management apprised that as a result of the imposition of levy on gas captive power plants it has moved its energy consumption to primarily LESCO for cost savings. Gas fired captive plant is now used only during peak hours.

The company is also in the process of adding a biomass fueled power plant of 37.2MW in addition to its 35 MW gas plant. It is expected that this new biomass plant will cater completely to the company’s current energy needs. The per unit cost of energy from the biomass plant is expected to be about 15-20% lower.

The biomass plant is expected to be commissioned in 18 months with construction having started in February 2025. ICL is also in the process of setting up a new and more efficient caustic flakes plant for export purposes. This plant is expected to come online by April 2026. Management estimated that its margin in the caustic soda segment is between 18% to 20% on average while the LABSA segment is between 8% and 10%.

In response to questions about change in duty structure and the viability of imports the management clarified that imports of caustic soda are not viable as the handling and storage of the liquid would require enhanced port infrastructure. The local price of caustic soda is currently PKR 155,000 per ton.

Going forward, the management was hopeful of growth in demand for its products as the economy begins rebounding especially in the personal care and detergent downstream sectors.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.