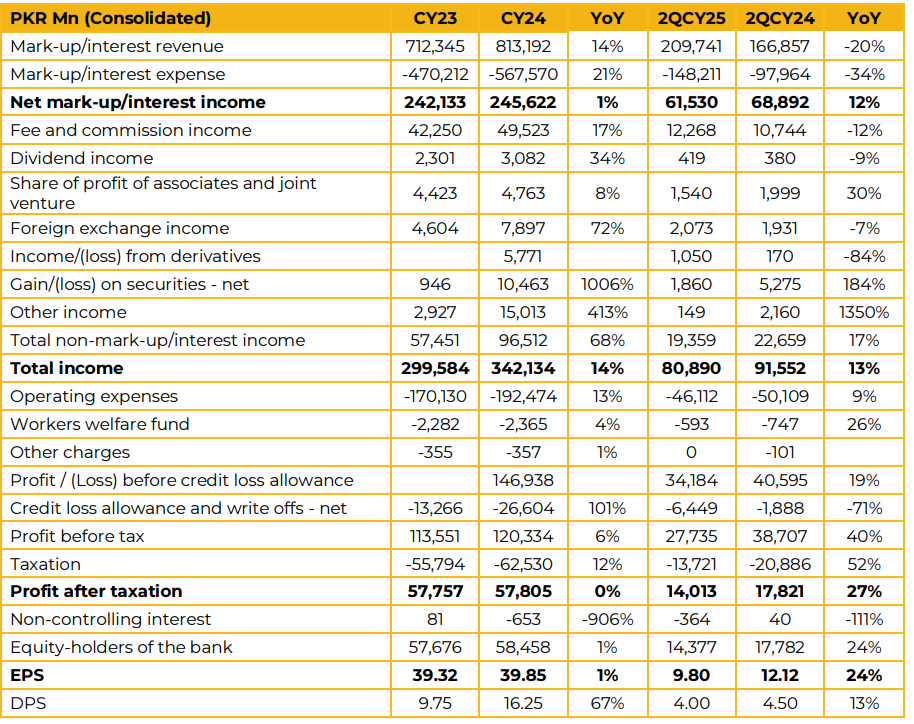

Habib Bank Limited reported consolidated earnings per share of PKR 12.12 in 2QCY25, up 24% from PKR 9.80 in 2QCY24. This translates into profit after tax of PKR 17.8 Bn compared to PKR 14.4 Bn in SPLY. The bank declared a dividend of PKR 4.5 per share in 2QCY25, up 13% from PKR 4.0 in 2QCY24. Total revenue in 2QCY25 reached PKR 91.6 Bn against PKR 80.9 Bn in 2QCY24, an increase of 13%.

This was primarily driven by a 12% increase in mark-up income from PKR 61.5 Bn in 2QCY24 to PKR 68.9 Bn in 2QCY25. The bank saw its total deposits rise from PKR 4.37 Trn at the end of CY24 to PKR 5.2 Trn at the end of 2QCY25, an increase of 19%. Current accounts now contribute 40.5% of the domestic deposit base with quarter-on-quarter growth of PKR 265 Bn. The management apprised that this growth was attributable to sustained efforts as well as the whole bank contributing to the growth as opposed to only branches.

Going forward, the management expects the deposit growth of the first half to continue in the second half of CY25. The bank targets to take the current accounts to 42% of deposits by end of CY25. Investments stood at PKR 4.3 Trn at June-2025, up 69% from PKR 2.5 Trn at the end of CY24. Management highlighted that out of its portfolio of investments of PKR 4.3 Trn, PKR 948 Bn is invested in fixed rate PIBs, PKR 2.17 Bn in PIB Floaters and PKR 766 Bn in T-Bills. Out of the fixed rate portfolio 2% will mature in this calendar year and another 5% in CY26. The bank’s cost to income ratio for 1HCY25 stood at 49.2% compared to 52.4% in 1HCY24. Management expects this downward trend to continue in the future. It noted that they wish to reduce this further by both cutting costs and by expanding their topline through the scalability of their infrastructure

Capital Adequacy Ratio stood at 17.9% up from 17.7% at the end of CY24. Advances to deposit ratio stood at 38% in Jun-25 down from 56% at the end of CY24.

The bank saw PKR 1 Bn profit in 1HCY25 from its subsidiary Habib Microfinance Bank against loss of PKR 3.6 Bn in SPLY. Moving forward, the management believes that the SBP will remain cautious for the rest of the calendar year due to an expected inflationary uptick near the end of the year along with uncertain global conditions with regards to tariffs and commodity prices

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.